Like It or Not, Dues Increases are the Appropriate Response to Inflationary Pressure.

Labor shortages and other inflationary pressures are budget busters. In the current environment, private club leaders are scrambling to cover current year...

.png?width=200&height=58&name=MicrosoftTeams-image%20(8).png "Club Benchmarking Logo png")

Labor shortages and other inflationary pressures are budget busters. In the current environment, private club leaders are scrambling to cover current year...

Over the coming weeks and months, clubs will be faced with lost revenue due to sustained closures and challenges related to retention of staff and members. Some clubs will emerge from...

by Steve Mona

Over the course of my 39-year career in the golf industry, I’ve earned a reputation as a guy who likes to stay busy. At the end of 2018, when I stepped back from my role as CEO of the World Golf Foundation, I accepted a new position as...

Originally published in NCA Club Director Magazine Fall 2018

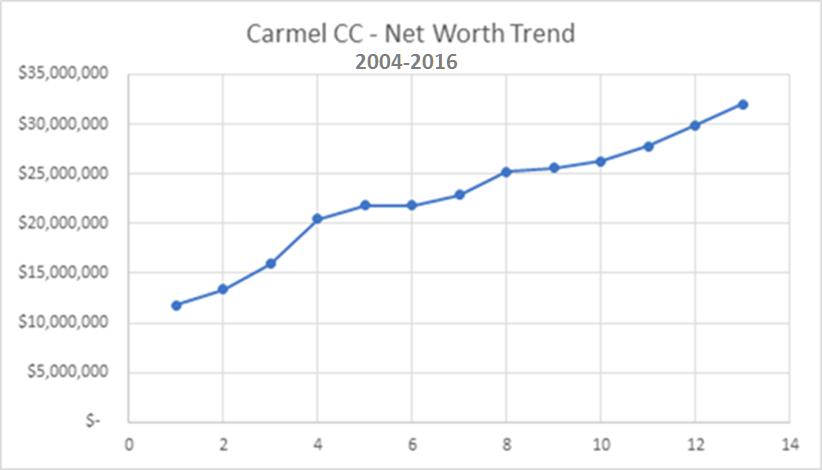

CLUB BENCHMARKING DATA REVEALS a “Tale of Three Cities” happening in the club industry, and we are deeply concerned about what appears to be a growing divergence. According to our...

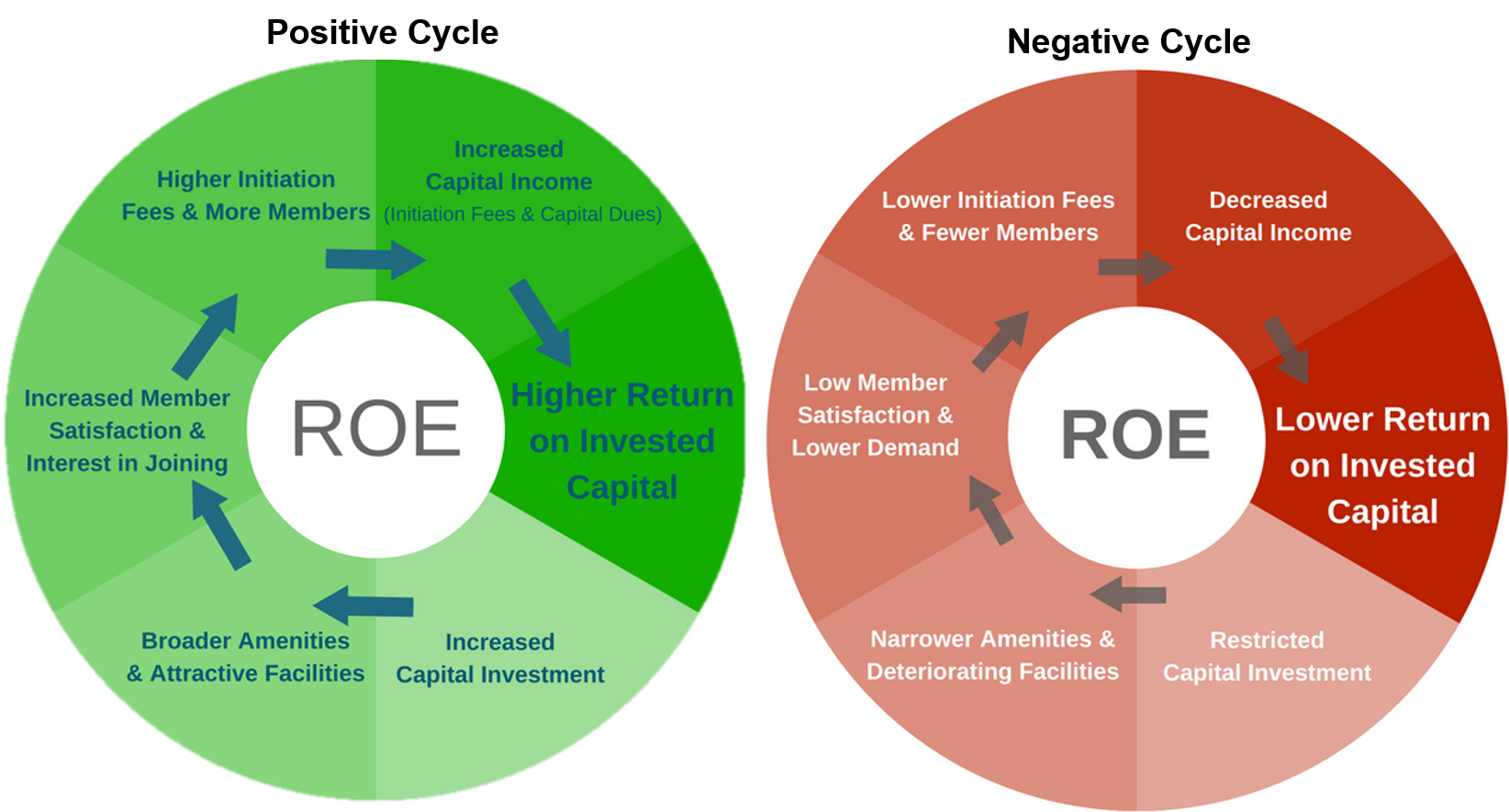

If just one rule could be instituted in every club boardroom with the goal of making the entire industry healthier, it would be this… Every time a Board member is tempted to bring up the subject of F&B profitability, they have to stop themselves and...

The private club industry in the United States has been a work in progress for more than 200 years. Clubs are deeply grounded in history and tradition, which may help to explain why the pace of change tends to be slower...

Every business charts the course for the coming year through the annual budget process, and private clubs are no exception. For many, the experience can be drawn out, difficult and fraught with struggles over...

Clubs share a common business model, but when it comes to more qualitative aspects like culture, each individual club is truly unique. At the highest level, a club’s culture is defined by factors such as history, mission,...

Armies of people study the dynamics of industries across the world. Bankers, investors, competitors, consultants—searching for clarity and insight on the factors...